Choosing a personal loan at Lloyds Bank often comes down to one crucial detail: the length of the repayment term.

Loan term lengths—whether short, medium, or long—carry major implications for monthly costs, total interest, and financial flexibility.

Understanding how Lloyds Bank structures its loan terms may be key for people considering their first loan or those thinking about refinancing.

This guide explores what actually matters when comparing loan term options—without the jargon you might find elsewhere.

Why Do Loan Terms Matter at Lloyds Bank?

Most prospective borrowers wonder just how much difference a few years in loan term length can make.

In truth, the choice between a shorter or longer term is rarely obvious and depends on what you want to achieve.

While a short-term loan can save money on interest, a longer term might make monthly budgeting easier.

Observing the trade-offs between these choices can help people align loans with their own priorities.

Common Term Lengths for Lloyds Bank Loans

At Lloyds Bank, borrowers usually find a selection of term lengths ranging from one year to seven years, though each offer is tailored.

The range provides a fair amount of choice, whether aiming for a quick payoff or spreading repayments over time.

Generally, longer terms are available for larger loan amounts, though approval depends on affordability checks and personal credit.

One to Three Years: Short-Term Options

Short-term loans at Lloyds Bank appeal to those who want to clear debt fast. Monthly payments are higher, but the benefit lies in minimizing interest paid overall.

Not everyone, however, finds it easy to manage the larger repayments month over month.

Four to Five Years: Standard Terms

Mid-length loans strike a balance between affordability and cost-efficiency. Repayments are manageable for most, while interest charges are still contained.

This window is among the more popular choices at Lloyds Bank, especially for moderate lending needs like car purchases or small renovations.

Six to Seven Years: Long-Term Loans

Longer-term loans lower the monthly financial pressure, freeing up cash flow for other commitments.

For significant expenses, like major home upgrades, this option makes repayments seem less daunting. The trade-off comes in the form of higher total interest, as the debt lingers over time.

Factors That Influence the Best Loan Term

No two borrowers are the same, which is why Lloyds Bank offers flexibility in choosing loan terms. Key factors to weigh include the loan’s size, monthly budget, total interest costs, and even future plans.

A sense of realism about changing life circumstances might be helpful too. Sometimes, what looks ideal at first could feel restrictive in practice.

Affordability and Monthly Repayments

The most pressing factor for many is whether the monthly repayment fits within existing expenses.

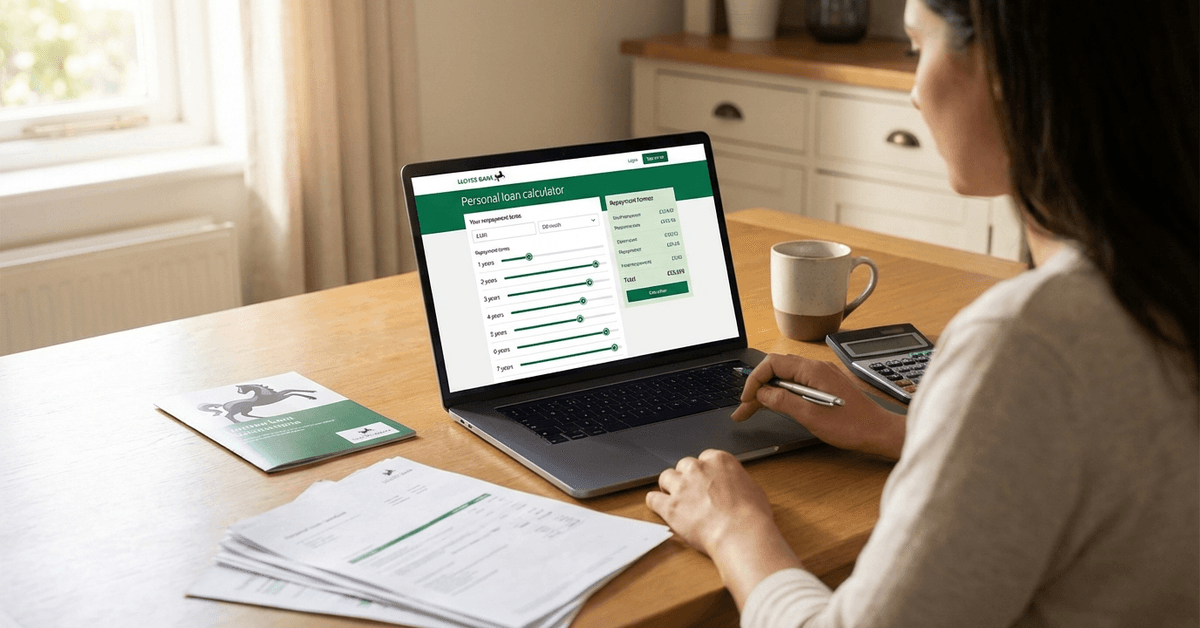

Using Lloyds Bank’s loan calculator (found on their website) gives a quick sense of monthly costs for various term choices. It’s helpful to remember budgets rarely stay static year over year.

Total Interest Paid Over Time

Shorter loan terms often mean less money spent on interest, but higher immediate payments. Longer terms stretch out debt, causing the total repayment amount to rise. It’s a subtle trade-off—pay now, or pay more later.

Personal Financial Plans and Security

Some prefer the peace of mind that comes with smaller monthly repayments, even if total interest is higher.

Others feel more comfortable with a faster debt payoff, accepting stricter monthly budgets for cost savings. There’s no right or wrong—just different priorities.

Representative Example from Lloyds Bank

To visualize how different terms affect costs, looking at a typical loan scenario can help. Lloyds Bank sometimes advertises representative APRs for loans of, for instance, £7,500 over 5 years.

Shortening that term could raise monthly outgoings but save hundreds in interest. Conversely, a seven-year loan lowers each payment but increases the total paid back. Individual quotes will differ, and the loan calculator or speaking with an adviser is recommended.

Comparing Lloyds Bank With Other Lenders

One common question is whether Lloyds Bank offers unique advantages for certain term lengths. While it’s true that some banks market ultra-short or very long loans, Lloyds typically focuses on reliability rather than extremes.

If flexibility matters, it can be wise to compare Lloyds’ offerings against top UK lenders such as Barclays, NatWest, or Halifax.

Rates, fees, and early repayment policies vary, so side-by-side comparisons are rarely wasted effort.

Tips for Navigating Term Length Choices

When in doubt, thinking through both immediate and long-term needs may help. Here are a few practical considerations to make the process less overwhelming:

- Estimate affordability with future changes in mind—job shifts, expenses, or growing families.

- Check if Lloyds Bank charges fees for early repayment; some flexibility can be reassuring.

- Factor in borrowing only the amount truly needed—larger loans tempt longer terms but cost more overall.

- Review the full loan agreement, not just headline rates or monthly repayment figures.

Legal and Financial Considerations for UK Borrowers

Loans from Lloyds Bank, like most UK providers, are subject to regulations that protect borrowers. Essential terms must be communicated clearly, and anyone considering a loan is given a cooling-off period. Credit checks apply.

It’s always worth evaluating total financial commitments; loans are a serious responsibility, and missed payments can impact credit for years to come.

Loan Term and Credit Score Impact

Oddly enough, the length of a loan can also influence your credit file. Timely repayments over a longer period may benefit a credit profile, but holding debt too long can count against you. As with the rest, moderation seems to help most.

What Happens at End of Term?

On completing a loan term, Lloyds Bank generally confirms account closure and remaining obligations, if any.

Early payment may be possible, sometimes even recommended if financial situations improve. Reading all documentation carefully can avoid surprises.

Is a Shorter or Longer Lloyds Loan Term Better?

There is ongoing debate over which approach is ‘best.’ Some prioritize freedom from debt at all costs, while others prefer the breathing room longer terms provide.

Personally, having taken both short and long-term loans at different life stages, it rarely felt like the same answer worked twice.

What’s certain: understanding all the implications makes a real difference to long-term satisfaction with a loan.

Final Thoughts

Choosing the right Lloyds Bank loan term depends on how you balance monthly affordability with total borrowing cost.

Shorter terms can save money on interest, while longer terms may make repayments easier to manage.

Your income stability, future plans, and comfort with debt all play a role in the best choice. Looking at the full loan picture before applying can help you avoid costly mistakes later.